")

")

Key Takeaways

- Italy’s AI market is rapidly expanding, creating major opportunities in AI search, generative AI, and GEO for early-moving businesses.

- AI Overviews and zero-click searches are reshaping SEO in Italy, making GEO, authority, and AI citations critical for visibility.

- Despite strong infrastructure, Italy’s low AI adoption and digital skills gap create a first-mover advantage for brands investing in AI strategies.

Italy is entering a defining phase in its digital evolution, where artificial intelligence is no longer an emerging concept but a rapidly scaling economic force reshaping how businesses operate, how consumers search, and how value is created across the economy. In 2026, the convergence of AI search, generative AI, and Generative Engine Optimisation (GEO) is fundamentally transforming Italy’s digital landscape—moving it from a traditional, Google-centric search ecosystem toward a multi-platform, AI-driven discovery environment. Against this backdrop, understanding the latest statistics, data points, and market trends is no longer optional for businesses operating in Italy—it is a strategic necessity.

The Italian AI market is expanding at an exceptional pace, with projections indicating growth from approximately US$4.65 billion in 2025 to over US$28 billion by 2031. This rapid expansion, supported by double-digit and even triple-digit growth rates across key segments such as generative AI, consumer AI, and enterprise AI software, highlights a market that is not only growing but accelerating. At the same time, Italy remains a mid-tier player within Europe—lagging behind leaders like Germany while maintaining a larger footprint than Southern European peers such as Spain. This positioning creates a unique dynamic: Italy is both an established digital economy and a high-growth opportunity market, where early adoption of AI search and GEO strategies can deliver disproportionate competitive advantages.

A major driver behind this transformation is the country’s accelerating investment in AI infrastructure. Multibillion-euro commitments from global hyperscalers, including Microsoft and AWS, alongside significant public sector funding through national initiatives and EU-backed programmes, are rapidly building Italy into a strategic AI infrastructure hub in the Mediterranean region. The expansion of high-density data centres, growing submarine cable connectivity, and increasing cloud capacity are enabling the computational backbone required for large-scale AI deployment. This infrastructure shift signals a deeper transition—Italy is evolving from a passive consumer of AI technologies into an active participant in the global AI ecosystem.

At the same time, Italy’s digital landscape presents a paradox of high connectivity but uneven adoption. With nearly 90% internet penetration, over 67 million mobile connections, and broadband access covering almost the entire connected population, the technical foundation for AI-powered search experiences is firmly in place. However, actual usage of generative AI tools remains comparatively low within the European Union. While awareness levels are high, a significant gap persists between understanding AI and integrating it into everyday behaviours. This awareness-to-adoption gap represents one of the most critical opportunities in the Italian market, particularly for brands that can educate, engage, and build trust with users as they transition toward AI-first search habits.

Consumer behaviour is already beginning to shift. AI platforms such as ChatGPT have gained substantial traction in Italy, reaching millions of monthly users and becoming a primary gateway for information discovery—particularly among younger demographics. Meanwhile, platforms like Google Gemini, Microsoft Copilot, Perplexity, and Claude are contributing to a fragmented but rapidly expanding AI search ecosystem. This diversification means that traditional search engine optimisation (SEO) strategies focused solely on Google are no longer sufficient. Instead, businesses must adopt a broader, multi-platform visibility strategy that aligns with how AI systems retrieve, summarise, and recommend information.

The rollout of Google AI Overviews in Italy marks a structural turning point in the country’s search ecosystem. Search is no longer defined purely by rankings and clicks, but increasingly by citations, summaries, and zero-click interactions. Data showing significant reductions in click-through rates, alongside a sharp rise in zero-click searches, underscores a fundamental shift in user behaviour. In this new paradigm, success is no longer measured solely by website traffic, but by a brand’s ability to be recognised, referenced, and trusted by AI systems. This shift is giving rise to Generative Engine Optimisation (GEO)—a new discipline that blends content authority, structured data, and real-time relevance to influence how AI models surface information.

For Italian businesses, this transformation is both disruptive and full of opportunity. On one hand, traditional content strategies—particularly those focused on broad, informational keywords—are facing declining visibility and engagement. On the other hand, highly specialised, authoritative, and data-rich content is increasingly being rewarded with greater prominence in AI-generated responses. The data clearly shows that factors such as content freshness, schema markup, domain authority, and expert attribution are becoming central to achieving visibility in AI search environments. As a result, GEO is rapidly emerging as one of the most important strategic capabilities for digital marketing teams operating in Italy.

At the enterprise level, AI adoption is accelerating, particularly among large organisations. However, small and medium-sized enterprises—which form the backbone of Italy’s economy—continue to lag behind. This uneven adoption highlights a critical structural challenge: while parts of the Italian economy are moving quickly toward AI integration, a significant portion remains in early experimentation stages. Coupled with a persistent digital skills gap and one of the lowest ICT graduate rates in the European Union, this creates both a constraint and an opportunity. Businesses that can bridge the gap between technology and practical implementation will be well-positioned to lead the next phase of Italy’s AI-driven growth.

Regulation also plays a defining role in shaping Italy’s AI landscape. As one of the first European countries to implement a comprehensive national AI law alongside the EU AI Act, Italy is establishing a clear regulatory framework governing how AI can be developed, deployed, and used. From workplace transparency requirements to strict penalties for misuse, the regulatory environment introduces both compliance obligations and long-term stability for businesses. Companies that proactively align their AI strategies with these regulations will gain a significant advantage in navigating the evolving legal landscape.

In parallel, Italy’s e-commerce sector—already valued at tens of billions of euros—is increasingly influenced by AI-driven discovery and decision-making. AI-powered search, recommendation engines, and conversational interfaces are reshaping how Italian consumers find and purchase products, particularly in mobile-first environments. With AI-assisted shopping showing significantly higher conversion rates and faster purchase journeys, the integration of AI search into e-commerce strategies is quickly becoming a key driver of revenue growth.

Globally, the rise of AI search platforms is reinforcing the urgency of these changes. With AI tools processing billions of queries daily and capturing a growing share of total search activity, the traditional boundaries between search engines and AI assistants are dissolving. For Italian businesses, this means competing not only within local markets but also within a global AI-driven discovery ecosystem where visibility is determined by algorithms that operate beyond geographic boundaries.

This comprehensive guide—“155 AI Search & GEO in Italy Statistics, Data & Trends in 2026”—brings together the most important data points, insights, and trends shaping this transformation. It provides a detailed, data-driven view of how AI is influencing Italy’s economy, digital behaviour, search landscape, and business strategies. For marketers, business leaders, investors, and technology professionals, these insights offer a roadmap to understanding where Italy stands today and where it is heading in the rapidly evolving world of AI search and generative optimisation.

As Italy continues its transition toward an AI-enabled economy, the key question is no longer whether AI will reshape search and business operations—but how quickly organisations can adapt to this new reality. Those that move early, invest strategically, and align with the emerging principles of GEO will not only navigate the disruption but also define the next generation of digital success in Italy.

But, before we venture further, we like to share who we are and what we do.

About AppLabx

From developing a solid marketing plan to creating compelling content, optimizing for search engines, leveraging social media, and utilizing paid advertising, AppLabx offers a comprehensive suite of digital marketing services designed to drive growth and profitability for your business.

At AppLabx, we understand that no two businesses are alike. That’s why we take a personalized approach to every project, working closely with our clients to understand their unique needs and goals, and developing customized strategies to help them achieve success.

If you need a digital consultation, then send in an inquiry here.

Or, send an email to [email protected] to get started.

155 AI Search & GEO in Italy Statistics, Data & Trends in 2026

A. ITALY AI MARKET SIZE & ECONOMICS

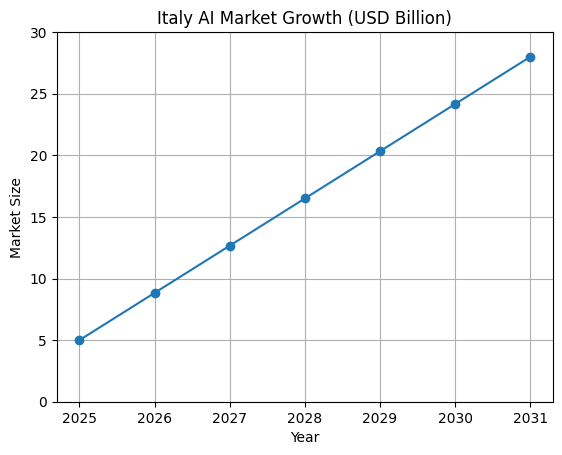

1. Italy’s AI market is on a steep growth trajectory, projected to reach US$4.65 billion in 2025 and expand at a 35.08% CAGR to US$28.26 billion by 2031, signalling strong long-term commercial opportunity for AI-driven businesses operating in the Italian market.

2. At €4.37 billion in 2025, Italy sits in the mid-tier of European AI markets — larger than Spain but well behind Germany — reflecting a market with significant headroom for growth compared to its northern neighbours.

3. Italy’s Consumer AI Market is projected to more than triple from USD 3.42 billion in 2024 to USD 16.41 billion by 2030, underscoring accelerating consumer-facing AI demand across sectors like retail, banking, and healthcare.

4. A forecast CAGR of 29.87% for Italy’s Consumer AI Market from 2025 to 2030 places it among the fastest-growing consumer tech segments in Southern Europe, making it an attractive destination for AI product investment.

5. Italy’s Generative AI market is expected to grow more than sixfold — from USD 547 million in 2024 to USD 3.3 billion by 2030 — driven by enterprise automation, content generation, and AI-powered search adoption.

6. Italy’s 3.2% share of the global generative AI market in 2024 is modest relative to its economic size as the third-largest Eurozone economy, suggesting that per-capita GenAI monetisation remains underdeveloped and ripe for expansion.

7. Italy’s AI software market grew 92% between 2019 and 2023 — from €260 million to roughly €500 million — demonstrating consistent market expansion even before the generative AI wave fully took hold.

8. Sector analysts estimate Italy’s broader AI market reached approximately €1.8 billion in 2025, driven primarily by enterprise adoption in manufacturing, finance, and logistics — three sectors where Italy has comparative economic strengths.

9. Conservative modelling by Market Research Future projects Italy’s AI market will reach USD 10.05 billion by 2035 at a 3% CAGR, which, while lower than other estimates, still represents a significant structural shift in how Italian businesses operate.

10. Italy’s data center market is forecast to grow from USD 6.4 billion in 2025 to USD 16.0 billion by 2034, driven by hyperscaler investment and rising demand for AI-ready compute infrastructure across Northern Italy.

11. Italy’s data center IT power capacity grew 17% year-on-year to 513 MW in 2024, reflecting the rapid physical buildout needed to support AI inference and cloud workloads at scale.

12. Italy’s data center market is projected to reach USD 6.22 billion by 2030 at a 12% CAGR, reinforcing the country’s emergence as a critical Mediterranean hub for AI infrastructure and cloud services.

B. MAJOR TECH INVESTMENT IN ITALIAN AI INFRASTRUCTURE

13. Microsoft’s €4.3 billion commitment to Italian cloud and AI data centers — its largest-ever investment in the country — positions Northern Italy as one of the most strategically important AI infrastructure zones in Europe.

14. Microsoft’s pledge to train more than 1 million Italians in AI skills by end of 2025 is a meaningful workforce development initiative, though it must be viewed alongside Italy’s systemic digital skills deficit to assess true structural impact.

15. AWS’s USD 1.2 billion investment in Italian AI-ready data center facilities, particularly in Lombardy, signals that hyperscalers view Italy as a long-term growth market, not merely a regulatory compliance zone.

16. Microsoft’s February 2026 commencement of construction at its high-density Bornasco data center marks a tangible milestone in Italy’s transition from AI consumer to AI infrastructure provider within Europe.

17. Italy’s government-approved plan for 14 new data centers representing €2.5 billion in investment demonstrates that public-sector commitment to AI infrastructure is moving beyond strategy into concrete capital allocation.

18. Italy’s Law 132/2025 earmarks up to €1 billion to support innovation in AI, cybersecurity, and quantum computing, representing one of the most direct public funding commitments to emerging technology in the country’s recent history.

19. With over 33 operational submarine cables and 5 more in the pipeline, Italy is rapidly cementing its role as Europe’s gateway data hub connecting the Mediterranean, North Africa, and the broader digital south.

20. The planned €3 billion Apto Lacchiarella Data Center Campus near Milan — covering 228,000 square meters — is poised to become one of the largest AI-capable data center facilities in Europe, dramatically increasing Italy’s compute density.

21. Italy’s PNRR allocation of €47 billion for digital initiatives, including a €520 million National Strategic Hub co-investment for sovereign cloud, represents one of the largest state-backed digital transformation programmes in EU history.

22. Italy’s €350 million República Digitale fund for digital upskilling through 2026 is a positive policy signal, though its impact will be judged by whether it meaningfully closes the gap with Northern European digital skill benchmarks.

C. ITALIAN INTERNET & DIGITAL LANDSCAPE

23. With 53.1 million internet users representing 89.9% of the population in late 2025, Italy has a near-universal online addressable market — making digital and AI search channels strategically essential for any brand targeting Italian consumers.

24. Italy’s 41.2 million social media user identities (69.7% penetration) confirm that social and search channels are deeply intertwined in Italian digital behaviour, with AI-generated content increasingly surfacing across both.

25. Italy’s 67.7 million active mobile connections — exceeding the total population at 114% — underscore the mobile-first nature of Italian internet usage, making mobile-optimised AI search experiences a non-negotiable priority.

26. With 98.6% of Italian mobile connections being broadband-capable, the technical infrastructure exists for AI-powered mobile search experiences to reach virtually every connected Italian — the bottleneck is adoption, not connectivity.

27. The approximately 5.95 million offline Italians represent a residual digital exclusion challenge, concentrated disproportionately among older populations and in the southern regions, that AI search adoption data must account for.

28. The finding that 73% of Italian citizens say digitalisation makes their lives easier is a strong signal of public receptiveness to digital tools — a sentiment that should, over time, translate into higher AI tool adoption rates.

29. Google’s over-90% search market share in Italy — peaking at 94.88% for all devices in March 2024 — makes Google AI Overviews the single most important AI search format for Italian SEO professionals to optimise for.

30. Google’s 88.27% desktop search share in Italy leaves a meaningful 11.73% for Bing, Yahoo, and other platforms, suggesting a small but non-trivial audience for Microsoft Copilot-integrated search experiences.

31. Google’s 98.6% mobile search share in Italy is effectively a monopoly, meaning mobile GEO strategy in Italy is almost entirely a Google Gemini and AI Overviews optimisation challenge.

32. Italy’s 614,044 Google Analytics-tracked websites reflect a digitally engaged business community, but relatively modest penetration compared to Italy’s ~4.4 million registered businesses, indicating large swathes of the economy have yet to fully embrace data-driven digital marketing.

D. ITALIAN AI TOOL ADOPTION & USAGE BY CONSUMERS

33. ChatGPT’s 8.8 million monthly active users in Italy — 20% of connected Italians — confirms it as the country’s dominant AI search and productivity tool, setting the baseline for any brand visibility strategy targeting Italian AI search users.

34. ChatGPT’s 35–37% penetration among Italian 18–24 year-olds reveals a generational adoption divide: younger Italians are normalising AI-first information retrieval, reshaping how the next generation of consumers will discover products and services.

35. Google Gemini and Microsoft Copilot trail ChatGPT in Italy with 2.8 million and 2.7 million monthly users respectively, indicating a fragmented AI search landscape where brands cannot afford to optimise for just one platform.

36. DeepSeek’s 716,000 users, Perplexity’s 270,000, and Claude’s 158,000 monthly Italian users represent smaller but growing platforms — particularly noteworthy as Perplexity monetises through AI search with cited brand references.

37. Italy’s 19.9% generative AI usage rate — second-lowest in the EU — is a dual signal: it reflects current underperformance in digital adoption, but also identifies Italy as a high-growth market where early movers in AI search can capture disproportionate share.

38. Italy’s generative AI adoption rate is nearly half that of Spain (38%) and France (37%), pointing to both a cultural and structural gap that Italian businesses and policymakers must urgently address to remain economically competitive.

39. Denmark (48.4%), Estonia (46.6%), and Malta (46.5%) lead EU generative AI adoption, demonstrating that smaller, highly digitised countries with strong education systems adapt fastest — a lesson Italy’s digital strategy should directly reference.

40. Bank of Italy survey data showing 75.6% AI awareness but only 36.7% actual usage reveals a significant awareness-to-adoption gap — suggesting that Italian consumers understand what AI is but have not yet integrated it into habitual behaviour.

41. Italy’s AI tool usage being skewed towards men, college graduates, and students mirrors global patterns of digital early adoption and highlights the social equity dimension of Italy’s AI rollout — less-educated and older populations risk being structurally excluded.

42. A 2% income return associated with AI usage in Italy — based on rigorous econometric analysis — is a modest but meaningful productivity signal, suggesting AI tools are beginning to create measurable labour market value even in early adoption stages.

43. Even among 16–24 year-olds, only 47.2% of young Italians used AI tools in 2025, one of the EU’s lowest youth AI adoption rates — a concerning indicator for Italy’s long-term digital competitiveness given that today’s young adults are tomorrow’s knowledge workforce.

44. Italy’s consistent co-ranking with Romania and Poland at the bottom of EU AI adoption tables is a structural concern rather than a data anomaly — persistent across multiple surveys, years, and demographic cohorts.

45. The gender gap in Italian AI usage, consistent with 21 of 27 EU member states, reflects broader digital participation inequalities that targeted AI literacy programmes must address to unlock Italy’s full AI productivity potential.

E. AI ADOPTION IN ITALIAN BUSINESS & ENTERPRISE

46. Business AI adoption in Italy doubling from 8.2% to 16.4% in just one year — with usage at just 5% two years prior — confirms an exponential S-curve dynamic is now underway in the Italian enterprise market.

47. Italy’s 18th EU ranking for business AI adoption, despite being the third-largest Eurozone economy, reflects a persistent digital transformation lag that structural factors — a dominance of SMEs, a manufacturing-heavy economy, and low ICT graduate rates — help explain.

48. The jump in AI adoption among large Italian enterprises (250+ employees) from 32.5% to 53% in one year is striking — large firms are crossing the adoption chasm, while SMEs continue to lag significantly.

49. Italian SMEs’ 14–15.7% AI adoption rate is a critical metric because SMEs constitute over 99% of Italian businesses and contribute approximately 67% of employment — meaning most of Italy’s economic output remains largely untouched by AI tools.

50. The North-South AI adoption divide in Italy — with North-West leading at 19.3% and the Mezzogiorno significantly behind — risks deepening existing regional economic inequalities if AI benefits are not deliberately distributed through policy and investment.

51. Italy’s improvement from 22nd to 18th in EU business AI adoption rankings between 2024 and 2025 is a genuine step forward, but closing the gap with leaders like Denmark, Finland, and the Netherlands will require sustained, multi-year investment.

52. Italian SME AI experimentation growing 50% year-on-year to 26.7% in 2025 is encouraging, though the gap between ‘tested AI’ and ‘strategically integrating AI’ remains wide for most small businesses.

53. With only approximately 9% of Italian SMEs using paid AI tools, the commercial AI market targeting small businesses in Italy is still nascent — representing a large, largely untapped B2B opportunity for AI solution providers.

54. Only 6% of Italian companies qualifying as ‘AI-driven’ while 42% remain fully ‘traditional’ reveals that even as usage metrics improve, strategic AI transformation remains the exception rather than the rule in Italian business culture.

55. EY’s finding that Italian professional AI tool usage jumped from 12% to 46% in one year demonstrates explosive individual adoption — but the critical challenge is translating personal productivity gains into organisation-wide strategic transformation.

56. The dominance of text writing (60%) and chatbots (47%) as AI use cases among Italian workers reflects early-stage adoption patterns — value extraction from AI in advanced applications like predictive analytics and process automation remains significantly underdeveloped.

57. Italy’s 16.4% business AI adoption versus the EU average of 20% confirms a structural gap — not a timing gap — that will require targeted industrial policy to address, particularly for the manufacturing and agriculture sectors that define the Italian economic backbone.

58. The fact that barely 9% of large Italian companies have structured AI governance — while 54% are still developing it — signals that Italy’s AI deployment is running ahead of its governance capabilities, creating potential regulatory and reputational risk.

59. Minsait’s finding of 3.2% current AI productivity gains rising to 4.3% within 24 months indicates that Italian businesses are beginning to see real returns on AI investment, reinforcing the business case for deeper integration.

60. The potential €115 billion in AI-driven productivity gains for Italian companies — if parameterised against Italy’s total corporate turnover — represents a macroeconomically significant prize that justifies ambitious public and private investment in AI readiness.

61. Nearly half of Italian companies (47.1%) using AI in production processes by 2025 represents a faster manufacturing-sector uptake than consumer adoption metrics suggest — reflecting AI’s practical, efficiency-driven appeal in Italy’s industrial heartlands.

62. More than half of Italian manufacturing companies (52%) using AI for workflow optimisation underscores that Italy’s famed industrial districts are increasingly embedding AI into precision manufacturing, logistics, and quality control processes.

63. Italy’s tech sector contribution of 6.8% to GDP — projected to hit 8.5% — reflects a digitally evolving economy, though it still trails UK (7.7%), Germany (estimated 9%), and Nordic economies where tech contributions consistently exceed 10%.

64. Management software adoption reaching 56% and advanced cloud services reaching 68.1% of Italian companies in 2025 indicates that the foundational digital infrastructure for AI integration — connectivity, cloud, and data management — is consolidating rapidly.

65. The fact that only 15% of Italian companies have a structured AI Act adaptation project — despite over half having launched awareness initiatives — reflects a dangerous gap between regulatory consciousness and operational compliance readiness.

F. AI DIGITAL SKILLS GAP IN ITALY

66. Italy’s 45.8% basic digital skills rate — 10 percentage points below the EU average and 34 points short of the 2030 target — is arguably the single greatest structural barrier to Italy realising its AI economic potential.

67. Southern Italy’s 36.1% basic digital skills rate — one of the lowest in any major EU economy’s region — makes the Mezzogiorno a profound digital exclusion zone where AI search adoption and business AI transformation face exceptional headwinds.

68. Italy’s 4% ICT specialist share of employment, below the EU’s 4.8% average, means Italian businesses face a persistent supply-side constraint in hiring the technical talent needed to build, deploy, and maintain AI systems.

69. Italy’s 1.4% ICT graduate rate — the lowest in the EU — is a structural time bomb: without a pipeline of domestically trained technical talent, Italy will remain dependent on imported technology and foreign expertise for its AI transformation.

70. Ranking 25th out of 27 EU member states for digital skills is not a temporary shortfall but a chronic systemic challenge, rooted in Italy’s historically low investment in digital education relative to its economic peers.

71. Italy’s 17th EU ranking for digital transformation combined with its 23rd ranking for general digitisation reveals an economy that has begun adopting digital tools at the sector level but has yet to achieve the population-wide digital fluency that underpins AI-native economies.

72. Italy’s failure to meet its own target of 70% basic digital skills penetration by 2025 — currently stuck at 45.8% — indicates that existing policy instruments are insufficient in scale and urgency to close the gap.

73. The net loss of 97,000 qualified young Italian workers over a decade — with emigration accelerating 21% year-on-year — is a brain drain directly relevant to AI capacity: the talent most likely to drive AI adoption is leaving.

74. Italy ranking 4th in Europe for generative AI startup development is a surprisingly strong finding that suggests pockets of genuine AI innovation exist, even as population-wide adoption lags significantly behind EU norms.

75. Italy’s AI software market growing 92% between 2019 and 2022 demonstrates that investment and commercial traction in AI are real and growing — the challenge is diffusing this momentum from tech hubs like Milan to the broader economy.

76. Italy’s mere 9 unicorn companies — disproportionately few for the third-largest Eurozone economy — reflects a startup ecosystem that struggles to scale, limiting the domestic development of AI products that could drive organic adoption.

77. Italy’s 152 edge nodes in 2024 represent a meaningful but insufficient distributed compute infrastructure for a country aiming to be a Mediterranean AI hub — edge expansion will be critical to enable low-latency AI applications outside major cities.

78. Italy’s potential to save €21.74 billion annually through AI in healthcare alone is a powerful policy argument: the country’s ageing population and healthcare system pressures make this one of the highest-ROI applications of AI available to Italian policymakers.

79. OECD projections of 0.2–0.8 percentage point annual productivity gains from AI for Italy over the next decade are meaningful in absolute terms — but trail the UK and US — confirming that Italy’s AI impact will be real but more gradual than frontier AI economies.

G. GOOGLE AI OVERVIEWS ROLLOUT & IMPACT IN ITALY

80. Google’s March 26, 2025, rollout of AI Overviews in Italy marks a structural turning point for Italian SEO: the paradigm has formally shifted from ranking for clicks to being cited in AI-generated summaries that many users never click through.

81. Informational content sites in Italy reporting 30–40% traffic reductions following AI Overviews rollout should serve as an urgent call to action for publishers, bloggers, and informational websites to pivot toward GEO-optimised content strategies.

82. The 15–45% visibility increase for hyper-specialised expert content in Italy’s AI Overviews era is a clear signal: depth, authority, and specificity are rewarded by AI systems, while broad, generalist content is increasingly commoditised.

83. The halving of traditional top-result CTR from 5.6% to 3.1% in Italy’s AI Overview-affected SERPs is not a temporary disruption — it is a permanent recalibration of how Italian users interact with search results pages.

84. AI Overviews appearing for 13% of global search queries — up from 6.49% in January 2025 — suggests that by end of 2026, the majority of high-intent Italian searches may surface an AI Overview, fundamentally altering the commercial value of organic rankings.

85. The 258% increase in AI Overviews for real estate queries and 273% for restaurants between January and March 2025 are particularly relevant for Italian local businesses, where sector-specific AI summaries are rapidly replacing traditional directory-style results.

86. With 88% of AI Overviews targeting informational queries, businesses that have built their Italian SEO strategies around educational and informational content face the greatest immediate disruption — and the greatest urgency to adapt.

87. AI Overviews now operating in over 200 countries, including Italy, means there is no market-specific exemption from this paradigm shift — Italian SEO teams cannot wait for a “localised” playbook; global GEO principles apply now.

88. Google AI Overviews reaching 1.5 billion monthly users globally as of January 2026 makes this the fastest-scaling search interface change in Google’s history — Italian brands with international traffic must optimise for a genuinely global AI audience.

89. The finding that 99.5% of AI Overview links come from top 10 organic results is strategically important: traditional SEO rank performance remains the foundational prerequisite for AI visibility, meaning GEO and SEO are complementary, not competing disciplines.

90. Seer Interactive’s finding of a 61% organic CTR drop and 68% paid CTR crash for AI Overview queries is among the most dramatic search behaviour data published to date — Italian advertisers must urgently reassess their paid search ROI assumptions.

91. Brands cited in AI Overviews earning 35% more organic clicks and 91% more paid clicks is a compelling commercial incentive for Italian brands to invest in becoming AI-cited sources — citation delivers compounding search advantage across both organic and paid channels.

92. A 34.5% average organic click reduction across 300,000 keywords analysed by Ahrefs is a statistically robust confirmation that AI Overviews systematically divert traffic away from source websites — a reality every Italian content publisher must now plan around.

93. Zero-click searches increasing from 56% to nearly 69% since AI Overviews launched means that for every 10 searches performed in Italy today, roughly 7 will end without a website visit — radically changing what ‘success’ looks like for Italian search strategies.

94. The finding that 93% of AI Mode searches end without a click — more than double the AI Overviews zero-click rate — signals that as AI search matures, the case for brand visibility over traffic volume becomes increasingly compelling for Italian marketers.

95. 39% of global marketers reporting traffic drops post-AI Overviews, with tech (44%) and travel (43%) most affected, is directly relevant to Italy’s tourism and technology sectors — two industries where AI Overviews are already materially reshaping how Italian businesses are discovered online.

H. GENERATIVE ENGINE OPTIMISATION (GEO) & AI SEARCH STRATEGY

96. The GEO market growing at a 50.5% CAGR from $848 million in 2025 to $33.7 billion by 2034 represents one of the most explosive commercial opportunities in digital marketing — and Italian agencies and consultancies that build GEO capability now stand to capture significant market share.

97. With 54% of US marketers planning GEO implementation within 3–6 months, Italian businesses risk falling further behind global competitors if they treat GEO as a future consideration rather than an immediate operational priority.

98. The reality that most SMBs — which dominate Italy’s economy — have not yet started GEO initiatives creates a genuine first-mover window in the Italian market, particularly for local and regional businesses willing to invest before competitors recognise the shift.

99. A 357% year-on-year increase in referral visits from AI platforms as of June 2025 confirms that AI search is no longer a niche traffic source — Italian brands that optimise for AI citation are accessing a fast-growing, high-intent audience segment.

100. The average AI search query being 23 words versus Google’s 4-word average demands a fundamental rethink of Italian keyword strategy: GEO content must answer full conversational questions and address nuanced user intent, not merely target short-tail keywords.

101. Users spending an average of 6 minutes per AI search session — 10x longer than on Google — suggests that AI search attracts higher-quality, more considered engagement, making AI-cited brands more likely to be remembered and acted upon.

102. Content earning 30–40% higher AI visibility when it includes citations, statistics, and quotations (Princeton GEO research) provides Italian content strategists with a clear, evidence-based framework: data-rich, well-cited content is the currency of GEO.

103. Pages updated within 60 days being 1.9x more likely to appear in AI answers establishes content freshness as a core GEO signal — Italian businesses must treat content maintenance as an ongoing operational commitment, not a one-time publishing activity.

104. Websites with author schema being 3x more likely to appear in AI answers makes author attribution — through structured markup — a high-ROI, low-cost GEO implementation priority for Italian content teams.

105. A 44% increase in AI search citations for sites using structured data and FAQ schema provides a concrete, measurable justification for Italian webmasters to prioritise schema implementation across their entire content inventory.

106. Schema markup adoption rising 35% from 2023 to 2026 globally indicates that technical SEO — specifically structured data — is becoming a mainstream GEO practice; Italian sites that have not yet implemented schema are increasingly at a competitive disadvantage.

107. The finding that 44.2% of all LLM citations come from the first 30% of text makes front-loaded content structure — leading with key facts, definitions, and data — a critical GEO writing discipline for Italian content creators targeting AI visibility.

108. Domain authority being the #1 predictor of AI citations, with high-traffic sites earning 3x more AI citations, confirms that brand trust and backlink authority accumulated through traditional SEO directly translates into GEO advantage — long-term brand building is not separable from AI search strategy.

109. The less-than-1-in-100 chance of ChatGPT or Google’s AI producing the same brand list for consecutive queries reveals the probabilistic, non-deterministic nature of AI citation — Italian brands must aim for broad AI visibility rather than relying on consistent ranking positions.

110. AI Overview content changing 70% of the time for the same query — and nearly half of citations being replaced when answers update — means Italian brands must continuously monitor and maintain their AI citation presence, not treat GEO as a set-and-forget activity.

111. Only 30% of brands remaining visible in back-to-back AI responses underscores the volatility of AI search citations and the need for Italian marketers to invest in building multi-platform presence across ChatGPT, Gemini, Perplexity, and AI Overviews simultaneously.

112. The 615x citation volume gap between the highest-citing (Grok: 27%) and lowest-citing (Claude: <1%) AI platforms demonstrates that different AI systems weight sources very differently — Italian brands need platform-specific GEO strategies, not one-size-fits-all approaches.

113. Grok’s 27% citation rate, Perplexity’s 13%, and Google AI Mode’s 9% collectively confirm a diversified, platform-specific AI citation landscape that Italian SEO strategies must map and track with dedicated GEO monitoring tools.

114. ChatGPT triggering web searches 59% of the time for local-intent prompts is highly relevant for Italian local SEO: appearing in ChatGPT’s real-time web-sourced responses requires the same local authority signals — NAP consistency, Google Business Profile, local citations — that traditional local SEO demands.

115. The convergence of SEO and GEO — evidenced by 99.5% of AI Overview sources coming from top-10 organic results — is the most strategically important finding in this report: Italian businesses do not need to choose between SEO and GEO; they must do both, integrated under a unified content authority strategy.

I. GLOBAL AI SEARCH PLATFORM STATISTICS

116. ChatGPT’s 883 million monthly users and 5.4 billion global monthly visits — exceeding Bing’s total — confirms that AI-native search is no longer a challenger to traditional search; it is a parallel ecosystem that Italian brands cannot afford to ignore.

117. ChatGPT processing 2 billion daily queries with an 80.49% AI chatbot market share establishes it as the de facto AI search standard against which Italian visibility strategies should first be measured and optimised.

118. AI tool monthly sessions now equating to 56% of all Google search globally signals that we are approaching a structural inflection point in how information is retrieved — a shift that Italian digital marketers must treat as permanent, not cyclical.

119. ChatGPT accounting for 20% of all search-related traffic worldwide in early 2026 means that one in five search interactions globally now bypasses traditional search engines — a share that will only grow as AI search interfaces improve.

120. Total search usage increasing 26% globally — combining search engines and LLMs — is an underreported but critical insight: AI search is not cannibalising traditional search so much as expanding the total volume of information queries, creating new visibility opportunities for Italian brands that master both channels.

121. Gartner’s prediction of a 25% drop in traditional search volume by 2026 provides strategic urgency: Italian businesses relying predominantly on Google organic traffic should begin diversifying their AI search presence now, before the projected volume decline materialises.

122. Gartner’s projection that 50% of all online searches will involve an AI assistant by 2028 is a two-year horizon that brings AI search from an emerging trend to a mainstream majority behaviour — Italian search strategies must be AI-ready before this tipping point, not after.

123. The projection that 36% of US adults will use GenAI as their primary search tool by 2028 is a leading indicator for Italian adoption trends, given Italy’s typical 2–3 year lag behind US digital behaviours — making 2030–2031 the likely Italian tipping point.

124. AI search visitors converting at 4.4x the rate of organic search visitors is the single most commercially compelling statistic for Italian e-commerce and lead-generation businesses: AI-referred traffic is qualitatively superior, justifying premium investment in GEO.

125. Generative AI driving a 4,700% year-on-year increase in US retail site traffic in July 2025 is a staggering data point that Italian e-commerce operators should study closely — AI-powered shopping discovery is growing exponentially, and Italian retailers need AI search presence to capture this channel.

126. 80% of B2B technology buyers trusting GenAI as much as traditional search when researching suppliers makes AI citation a critical component of Italian B2B marketing and account-based strategy, particularly for Italian tech exporters targeting international buyers.

J. ITALY’S AI REGULATION & LEGAL FRAMEWORK

127. Italy enacting Law 132/2025 — the EU’s first comprehensive national AI framework — in October 2025 positions Italy as a regulatory pioneer within Europe, giving businesses operating in Italy both first-mover compliance obligations and the clarity of a defined legal operating environment.

128. Italy’s October 2026 deadline for implementing decrees under Law 132/2025 means Italian businesses have a narrow window to align their AI training data practices, algorithmic processes, and compliance structures before enforceable rules take full effect.

129. Fines of up to €1,500 per employee for employers failing AI workplace transparency obligations under Italy’s AI Law make HR and workforce AI policies a pressing compliance priority — particularly for Italy’s large manufacturing and service sector employers.

130. Maximum fines of €774,685 and potential business disqualification under Italy’s AI Law establish a meaningful deterrent regime — the regulatory risk of AI non-compliance in Italy is now commercially significant and not merely theoretical.

131. Italy’s age-differentiated AI consent framework — requiring parental consent for under-14s and informed self-consent for 14–18 year-olds — introduces specific compliance obligations for any AI-powered product or search experience targeting younger Italian audiences.

132. Italy’s criminal penalties of 1–5 years for unlawful deepfake dissemination send a clear signal to content creators, marketers, and AI tool operators: generative AI’s creative capabilities come with serious legal accountability in the Italian jurisdiction.

133. Italy’s 2023 ChatGPT ban — the first by any Western country — established Italy as a serious GDPR enforcer in the AI space, a precedent that continues to shape how global AI companies approach data governance when targeting Italian users.

134. The EU AI Act’s maximum fine of €35 million or 7% of global turnover — the world’s strictest AI penalty regime — applies fully in Italy, meaning multinational brands operating AI systems for Italian audiences must treat EU AI compliance as a board-level risk management issue.

135. Italy’s forthcoming healthcare AI data guidelines reflect the sensitivity of medical applications and the particular scrutiny that AI systems processing health data will face — a relevant consideration for Italian health tech and digital health marketing sectors.

136. Italy’s prohibition on full AI delegation of professional services — including legal and medical — with mandatory transparency disclosures reflects a human-in-the-loop philosophy that will shape how AI-assisted professional content is disclosed in Italian search and marketing contexts.

137. The creation of a National Observatory on AI in the workplace under Italy’s AI Law is a forward-looking governance mechanism that acknowledges AI’s employment impact and creates an institutional body capable of recommending adaptive policy as AI deployment evolves.

K. ITALY’S NATIONAL AI STRATEGY 2024–2026

138. Italy’s AI Strategy 2024–2026 anchored around three macro-objectives — adoption support, sector application, and enabling conditions — provides a coherent policy architecture that, if funded and executed, could meaningfully accelerate the country’s AI transformation trajectory.

139. The explicit framing of Italy’s AI strategy around ‘anthropocentric, reliable, and sustainable AI’ aligns with EU values but also reflects a culturally Italian emphasis on human dignity and craftsmanship — a values system that may inform how Italian users engage with AI search tools over time.

140. The AI Strategy’s focus on manufacturing, agri-food, tourism, and finance maps directly onto Italy’s genuine economic strengths — a strategically coherent choice that maximises the likelihood of AI delivering measurable GDP impact in sectors where Italy already has global competitive advantage.

141. Italy’s digital transformation budget of €62.3 billion (2.84% of GDP) represents a substantial national commitment — but execution quality, not budget size, will determine whether Italy closes its digital gap with Northern European peers.

142. Italy’s AI strategy priority to develop domestic AI systems and reduce foreign technology dependence reflects a broader European digital sovereignty agenda — one with direct implications for which AI search platforms gain regulatory favour in the Italian market over time.

143. Lombardy and Lazio accounting for over 45% of Italy’s ICT expenditure confirms that AI investment and innovation remain heavily concentrated in Milan and Rome, creating a geographic concentration risk for national AI strategy effectiveness.

144. Italy’s AI software market growing 92% from 2019 to 2023 before the generative AI wave demonstrates that the current growth surge is built on a pre-existing foundation of genuine AI investment — not simply hype-driven budget allocation.

L. ITALY E-COMMERCE & AI SHOPPING BEHAVIOUR

145. Italy’s €85.4 billion e-commerce market growing toward €100 billion by 2029 is a large and growing commercial context in which AI-powered search and product discovery will play an increasingly decisive role in determining which brands win online.

146. Italy’s 30.2 million e-commerce users at 50.9% population penetration in 2025 indicates that online shopping has reached majority status in Italy — but the remaining 49.1% represents a substantial growth frontier, particularly as AI-powered shopping experiences lower friction for hesitant buyers.

147. 39 million Italians incorporating online channels into their customer journey in December 2023 — including those who research online but buy in-store — underscores the importance of AI search optimisation even for businesses that primarily serve physical retail customers.

148. Italy’s e-commerce user penetration projected to reach 57.2% by 2030 suggests steady but not explosive growth — the implication for AI search is that Italian online commerce will incrementally absorb AI discovery tools rather than experiencing a sudden behavioural discontinuity.

149. Italy’s 39% cross-border e-commerce share means a significant portion of Italian online shopping involves non-Italian retailers — a competitive pressure that makes Italian domestic brands’ AI search visibility internationally, not just domestically, strategically important.

150. Clothing and footwear leading Italian e-commerce at 35% of purchases is highly relevant for GEO: fashion is a category where AI visual search, style recommendations, and natural language product discovery are advancing rapidly, creating sector-specific GEO opportunities for Italian fashion brands.

151. Smartphones driving 47% of Italian cross-border e-commerce purchases reinforces the primacy of mobile AI search experiences — Italian retailers targeting cross-border buyers must optimise their mobile AI search presence and ensure AI-friendly product schema is mobile-responsive.

152. AI chat driving a 4x conversion rate improvement (12.3% vs 3.1%) for e-commerce is a headline commercial finding for Italian online retailers: deploying AI chat and ensuring AI search citation is not just a marketing consideration but a direct revenue lever.

153. AI-assisted shoppers completing purchases 47% faster — 8 minutes versus 15 minutes — demonstrates that AI search reduces purchase friction in ways that directly benefit Italian e-commerce conversion rates, customer experience scores, and operational efficiency.

154. Italy’s below-average use of AI tools for formal education mirrors the country’s broader adoption lag and highlights an educational system that has yet to integrate AI-assisted learning into mainstream curriculum — a gap with long-term implications for AI literacy and AI search competence among future Italian consumers and workers.

155. EY’s finding that Italian professional AI tool usage quadrupled from 12% to 46% in just one year is the most optimistic data point in this entire dataset — it suggests that when Italian professionals are exposed to and supported in using AI tools, adoption can be rapid, non-linear, and transformative.

Conclusion

Italy’s AI landscape in 2026 stands at a critical inflection point—one defined not by uncertainty, but by acceleration, imbalance, and opportunity. The data presented across these 155 statistics makes one conclusion unmistakably clear: artificial intelligence is no longer a peripheral trend in Italy’s digital economy. It is becoming a foundational layer that is reshaping how information is discovered, how businesses compete, and how value is created across nearly every sector.

From a macroeconomic perspective, Italy’s AI market is expanding rapidly, with strong projections across enterprise AI, consumer AI, and generative AI segments. While the country still sits behind leading European economies such as Germany, the growth trajectory signals that Italy is transitioning from a mid-tier digital market into a high-growth AI opportunity zone. This combination of scale and underdevelopment is particularly important—it creates a rare window where businesses that invest early in AI capabilities and visibility strategies can capture disproportionate market share before adoption becomes saturated.

At the infrastructure level, Italy is undergoing a profound transformation. Massive investments from global hyperscalers, alongside significant public funding and policy support, are laying the groundwork for a robust AI ecosystem. The expansion of data centers, cloud capacity, and international connectivity is not only enabling domestic AI adoption but also positioning Italy as a strategic AI infrastructure hub bridging Europe, the Mediterranean, and emerging digital markets. This shift signals a deeper evolution: Italy is no longer just consuming AI technologies—it is increasingly capable of hosting, scaling, and exporting them.

However, the most defining characteristic of Italy’s AI journey is the gap between potential and execution. Despite high internet penetration, strong mobile connectivity, and growing awareness of AI technologies, actual adoption remains uneven across the population and business landscape. The persistent digital skills gap, low ICT graduate output, and regional disparities—particularly between Northern Italy and the Mezzogiorno—represent structural constraints that could limit the country’s ability to fully capitalise on its AI momentum. These challenges are not temporary; they are systemic, and addressing them will require sustained investment in education, workforce development, and inclusive digital policies.

From a behavioural standpoint, Italian consumers are beginning to shift toward AI-driven search and discovery, but this transition is still in its early stages. Platforms such as ChatGPT have already established themselves as major entry points for information retrieval, especially among younger users, while Google continues to dominate traditional search. At the same time, the emergence of alternative AI platforms—including Gemini, Copilot, Perplexity, and others—has created a fragmented yet rapidly evolving search ecosystem. This fragmentation fundamentally changes how brands must approach visibility: success is no longer about ranking in a single search engine, but about being present, cited, and trusted across multiple AI systems simultaneously.

The introduction of Google AI Overviews in Italy represents perhaps the most disruptive shift in the entire dataset. The transition from click-based search to AI-generated answers has already begun to erode traditional traffic models, with zero-click searches rising sharply and click-through rates declining across both organic and paid channels. For businesses and publishers, this is not a temporary fluctuation—it is a structural recalibration of how search works. The implication is profound: visibility, authority, and brand recognition are becoming more valuable than raw traffic volume.

This is where Generative Engine Optimisation (GEO) emerges as a defining discipline for the next era of digital strategy. The data clearly demonstrates that AI systems prioritise content that is authoritative, well-structured, frequently updated, and supported by credible data and citations. Traditional SEO foundations—such as domain authority and high-quality content—remain essential, but they are no longer sufficient on their own. GEO requires a more advanced approach, one that integrates technical optimisation, content strategy, and brand trust into a unified framework designed specifically for AI-driven discovery environments.

For Italian businesses, this shift presents both a challenge and a significant opportunity. On one hand, companies that continue to rely solely on traditional SEO tactics risk losing visibility as AI systems increasingly mediate user interactions. On the other hand, those that proactively adopt GEO strategies—by investing in structured data, expert-led content, multi-platform presence, and continuous content optimisation—can position themselves as authoritative sources within AI-generated responses. This is particularly important in a market like Italy, where overall AI adoption remains relatively low, creating a first-mover advantage for organisations willing to lead the transition.

At the enterprise level, the data reveals a dual-speed economy. Large organisations are rapidly integrating AI into their operations, driving efficiency gains and productivity improvements, particularly in sectors such as manufacturing, finance, and logistics. Meanwhile, small and medium-sized enterprises—which form the backbone of Italy’s economy—are progressing more slowly, often limited by resource constraints, lack of expertise, and uncertainty about implementation. This gap is critical because it means that a large portion of Italy’s economic output remains under-optimised for AI, representing both a risk to national competitiveness and a substantial opportunity for AI solution providers targeting the SME segment.

Regulation further adds complexity to the Italian AI landscape. With the introduction of national AI legislation and the broader framework of the EU AI Act, Italy is positioning itself as a leader in AI governance. While this creates additional compliance requirements for businesses, it also provides a level of clarity and stability that can support long-term investment. Companies that integrate compliance into their AI strategies from the outset will be better positioned to navigate this evolving regulatory environment and build trust with both consumers and regulators.

The implications for e-commerce and digital commerce are equally significant. As AI-driven search and recommendation systems become more prevalent, the way Italian consumers discover and purchase products is changing rapidly. AI-assisted shopping experiences are already demonstrating higher conversion rates and faster decision-making processes, particularly in mobile environments. For Italian retailers, this means that visibility within AI search ecosystems is no longer just a marketing concern—it is a direct driver of revenue and competitive positioning.

On a global level, the rise of AI search platforms reinforces the urgency of these changes. With AI tools capturing an increasing share of search activity and user engagement, the digital landscape is expanding rather than contracting. This expansion creates new opportunities for Italian brands to reach both domestic and international audiences, but only if they adapt to the new rules of AI-driven discovery. The convergence of traditional search and AI search into a unified ecosystem means that businesses must adopt a holistic strategy that addresses both channels simultaneously.

Ultimately, the Italian AI market in 2026 can be defined by three core dynamics: rapid growth, structural gaps, and strategic opportunity. Infrastructure is advancing quickly, awareness is high, and enterprise adoption is accelerating—but skills, widespread usage, and SME transformation remain key bottlenecks. This imbalance is precisely what creates opportunity. Markets that are already fully mature offer limited room for differentiation, but Italy’s current position allows forward-thinking organisations to establish leadership before the rest of the market catches up.

The path forward is clear. Businesses operating in Italy must move beyond experimentation and begin integrating AI into their core strategies—whether in marketing, operations, customer experience, or product development. At the same time, they must recognise that visibility in the age of AI is no longer about ranking alone, but about being understood, trusted, and cited by intelligent systems. GEO is not a future concept; it is an immediate requirement for any organisation that wants to remain competitive in an AI-driven search environment.

In conclusion, Italy’s AI search and GEO landscape is not just evolving—it is being redefined. The companies that succeed in this new environment will be those that combine technological adoption with strategic clarity, content authority, and a deep understanding of how AI systems interpret and prioritise information. As the data in this report demonstrates, the shift is already underway. The only remaining question is how quickly businesses will adapt—and whether they will lead or follow in the next chapter of Italy’s digital transformation.

If you are looking for a top-class digital marketer, then book a free consultation slot here.

If you find this article useful, why not share it with your friends and business partners, and also leave a nice comment below?

We, at the AppLabx Research Team, strive to bring the latest and most meaningful data, guides, and statistics to your doorstep.

To get access to top-quality guides, click over to the AppLabx Blog.

People also ask

What is the current size of the AI market in Italy in 2026?

Italy’s AI market is rapidly expanding, with projections showing strong multi-billion-dollar growth driven by enterprise adoption, generative AI, and digital transformation initiatives across key industries.

How fast is the AI market growing in Italy?

Italy’s AI market is expected to grow at a high CAGR, with forecasts exceeding 30% annually, reflecting strong demand for AI-driven solutions across sectors.

What is Generative Engine Optimisation (GEO)?

GEO is the practice of optimising content to be cited and surfaced in AI-generated answers, focusing on authority, structured data, and relevance rather than traditional rankings.

Why is GEO important for Italy in 2026?

With AI search growing rapidly in Italy, GEO is essential for businesses to maintain visibility as users increasingly rely on AI-generated summaries instead of traditional search results.

How is AI search changing SEO in Italy?

AI search shifts focus from clicks to citations, requiring brands to prioritise authority, expertise, and structured content to appear in AI-generated responses.

What are Google AI Overviews and why do they matter?

Google AI Overviews provide AI-generated summaries directly in search results, reducing clicks and making content citation more important than traditional rankings.

Is AI adoption high in Italy compared to other EU countries?

Italy’s AI adoption is lower than many EU peers, highlighting a gap but also a significant growth opportunity for early adopters.

Which AI tools are most popular in Italy?

ChatGPT leads AI tool usage in Italy, followed by platforms like Google Gemini, Microsoft Copilot, and emerging AI search tools.

How many Italians use AI tools today?

Millions of Italians use AI tools monthly, but overall adoption remains relatively low compared to awareness, indicating strong future growth potential.

What industries are driving AI growth in Italy?

Manufacturing, finance, logistics, retail, and healthcare are key sectors driving AI adoption and investment in Italy.

How is AI impacting Italian businesses?

AI is improving productivity, automating processes, and enhancing decision-making, particularly in larger enterprises and industrial sectors.

Are Italian SMEs adopting AI quickly?

SMEs are adopting AI more slowly than large enterprises, creating a major opportunity for AI solution providers targeting small businesses.

What is the biggest barrier to AI adoption in Italy?

The digital skills gap is the primary challenge, limiting widespread AI adoption across both consumers and businesses.

How does Italy’s digital infrastructure support AI growth?

High internet penetration, strong mobile connectivity, and expanding data centers provide a solid foundation for AI adoption and growth.

What role do data centers play in Italy’s AI ecosystem?

Data centers enable AI processing and cloud services, with major investments positioning Italy as a regional AI infrastructure hub.

How is AI changing online search behaviour in Italy?

Users are shifting toward conversational, long-form queries and relying more on AI-generated answers rather than traditional search results.

What is zero-click search and why is it increasing?

Zero-click search occurs when users get answers directly from search pages, and it is rising due to AI Overviews and AI search tools.

How should businesses adapt to AI search in Italy?

Businesses must focus on GEO, create authoritative content, use structured data, and optimise for multiple AI platforms.

What content performs best in AI search results?

Content that is data-driven, well-structured, frequently updated, and backed by credible sources performs best in AI-generated answers.

Does traditional SEO still matter in Italy?

Yes, traditional SEO remains essential, as strong rankings and domain authority increase the likelihood of being cited in AI responses.

What is the relationship between SEO and GEO?

SEO and GEO are complementary, with SEO building authority and GEO ensuring visibility in AI-generated search results.

How is AI affecting website traffic in Italy?

AI search is reducing traditional traffic through zero-click results, requiring businesses to shift focus toward visibility and brand presence.

What is the future of AI search in Italy?

AI search is expected to become mainstream, with increasing adoption and deeper integration into everyday digital experiences.

How does AI impact e-commerce in Italy?

AI enhances product discovery, improves recommendations, and increases conversion rates through faster and more personalised shopping experiences.

Is mobile important for AI search in Italy?

Yes, Italy is a mobile-first market, making mobile optimisation critical for AI search visibility and user engagement.

What is the role of structured data in GEO?

Structured data helps AI systems understand and extract content, significantly increasing the chances of being cited in AI answers.

How often should content be updated for GEO?

Content should be updated regularly, ideally within 60 days, to improve relevance and increase visibility in AI search results.

What are the key ranking factors for AI citations?

Authority, freshness, structured data, expert attribution, and content depth are key factors influencing AI citations.

How is Italy’s AI regulation impacting businesses?

Strict AI laws and EU regulations require businesses to ensure compliance, particularly in data usage, transparency, and AI deployment.

What is the biggest opportunity in Italy’s AI market?

The biggest opportunity lies in early adoption of AI and GEO strategies, allowing businesses to gain a competitive edge in a rapidly evolving market.

Sources

Statista Market Forecast

Cargoson

Statista

Next Move Strategy Consulting

Grand View Research

Horizon Databook

Rome Business School

Junto.space Analysis

Market Research Future

IMARC Group

Futurism

Data Center Observatory Milan Polytechnic

CleanBridge

ResearchAndMarkets

GlobeNewsWire

Microsoft News Center Italy

Microsoft

PYMNTS

Italy Data Center Market

We Build Value

Norton Rose Fulbright

Italy AI Law

BusinessWire

Black Ridge Research

Digital Skills and Jobs Platform

DataReportal

European Commission

Italy Digital Decade Country Report

StatCounter

99firms

Electroiq

SQ Magazine

Vincenzo Cosenza

Audicom

Audiweb

Italian Facts

Eurostat

Euronews

Bank for International Settlements

BIS

Format Research

ISTAT

Il Sole 24 ORE

Italiaonline Research

AIdIA

altermAInd Research

EY Italy AI Barometer

Minsait

Nucamp

Tech Sector Analysis

Reuters

Italy National Strategy for Digital Skills

Republica Digitale

OECD

Evergreen.media

PPC.land

Digidop

Google I O Analysis

Semrush

HT and T Consulting

seoClarity

Search Engine Land

Superlines

Seer Interactive

Dataslayer

Ahrefs

SE Ranking

Digital Bloom

Position Digital

Fractl

Dimension Market Research

eMarketer

Enrich Labs

Similarweb

Brosch Digital

LLMrefs

Princeton University

BrightEdge

Growth Memo

AirOps Research

Nectiv

Exposure Ninja

Graphite

Gartner

Rep AI

Adobe Digital Insights

Forbes

Ecom Lens

Responsive Buyer Intelligence

Cleary Gottlieb

White and Case

Global AI Regulatory Tracker

K and L Gates

Legal Nodes

Covington

Global Policy Watch

Orrick

CSO Online

ScienceDirect

National Law Review

Interoperable Europe Portal

Landmark Global

Ecommerce Europe

Image Sizes in 2024: The Ultimate Guide")

{kind=link}